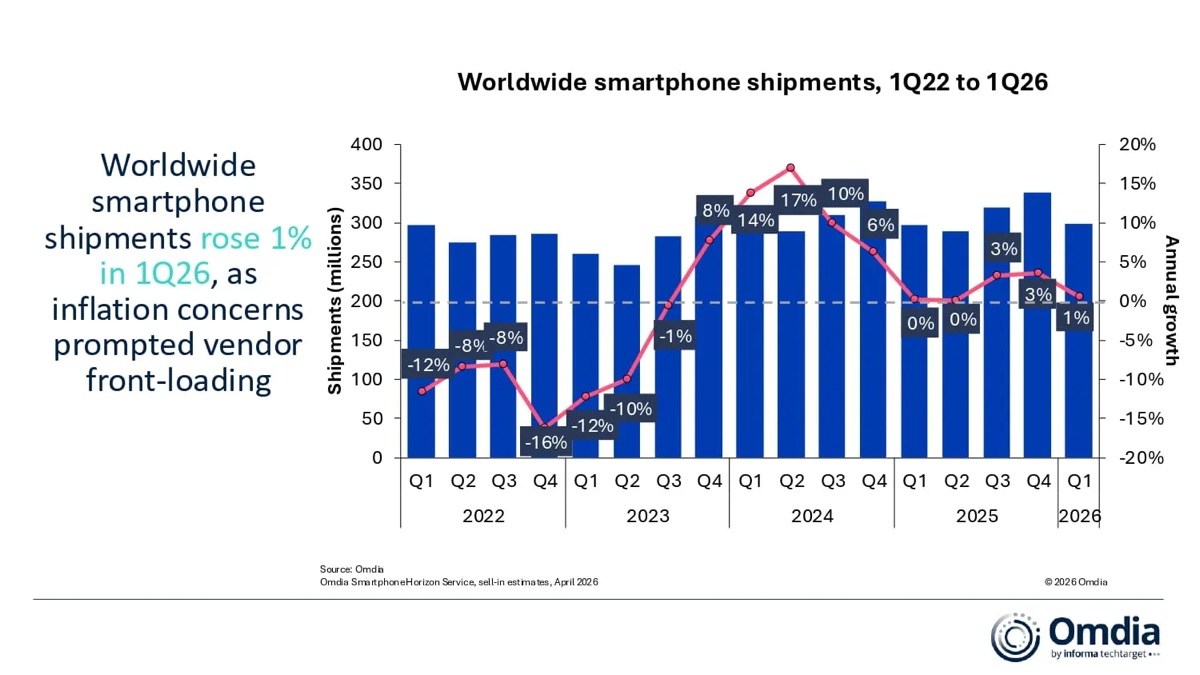

Despite the ongoing memory chip crisis, Omdia reported a 1% rise in global smartphone shipments for Q1. Total shipments during the first three months of the year reached 298.5 million units, fueled by vendor front-loading. This is when smartphone companies strategically push inventory volumes in anticipation of rising component costs.

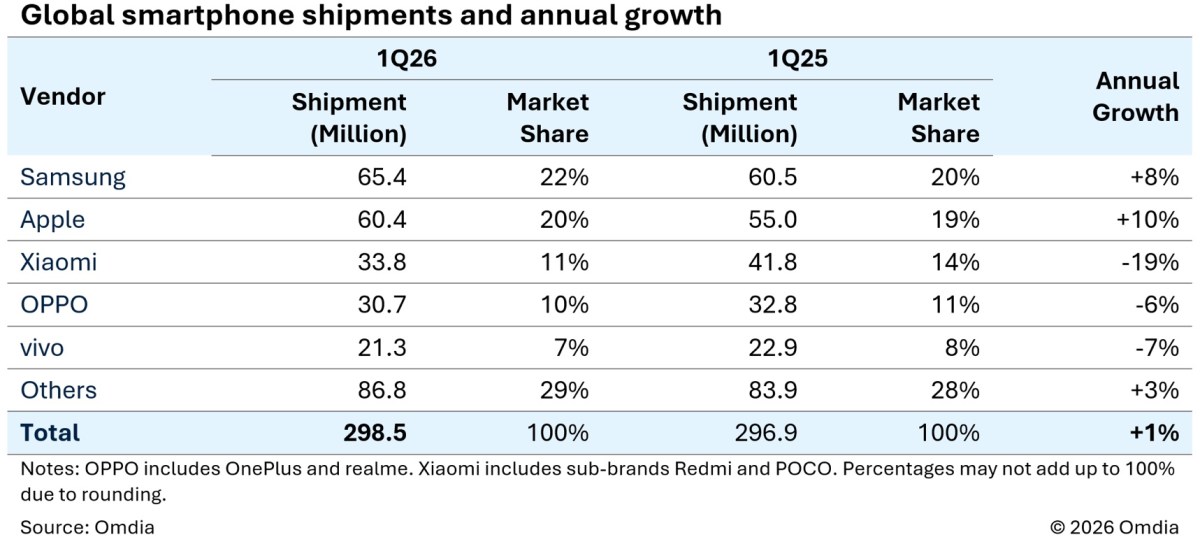

Samsung regained the title as the world’s number one smartphone brand, thanks to 65.4 million shipments for the period, which represents an 8% rise compared to the same time last year. The Galaxy S26 series is seeing strong demand, and the recently launched Galaxy A37 and Galaxy A57 are also key contributors to Samsung’s 22% market share.

Apple was the second leading brand for the period with 60.4 million shipments (up 10% YoY) while controlling an estimated 20% of the global market. Demand for the iPhone 17 series has remained strong, and the report also highlights higher-than-anticipated user interest for the iPhone 17e across Europe and Japan. The flagship iPhone 17 Pro and 17 Pro Max also edged out their predecessors with an impressive 42% rise in demand across China.

Xiaomi (including Redmi and Poco) came in third place with 33.8 million shipments and an 11% market share, but it also experienced the largest annual drop (-19%) in shipments in the top five. Rising component costs have effectively squeezed Xiaomi’s margins.

Oppo (including OnePlus and Realme) came in fourth with 30.7 million shipments and a 10% market share, while vivo ranked fifth with 21.3 million shipments and a 7% market share.

Looking ahead, Omdia analysts predict turbulent times with a period of adjustment following the supply-side push by vendors. Elevated channel inventory and generally weak consumer demand will be key factors shaping the global smartphone market heading into the second half of 2026.